U.S. Hardwood Veneer and Plywood Market. Analysis And Forecast to 2030

Get instant access to more than 2 million reports, dashboards, and datasets on the IndexBox Platform.

View PricingHardwood Veneer and Plywood Market - Rising Consumption in Housing and Commercial Building Sectors Continue to Drive the U.S. Hardwood Veneer and Plywood Market

Photo: © Tethys Imaging LLC / Bigstockphoto

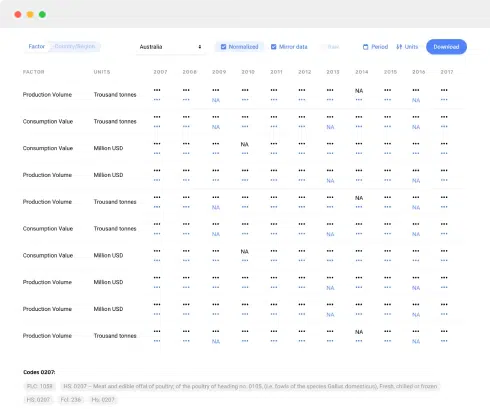

From 2007 to 2015, U.S. hardwood veneer and plywood market showed mixed dynamics. A significant drop in 2009 was followed by steady growth over the next six years. Finally, the market value reached X million USD in 2015. An increase in U.S. hardwood veneer and plywood market was supported by the growth of the housing and commercial building sectors and, as a result, the furniture sectors increased as well. That upward trend is likely to continue in the medium term. Strong employment is the driver of market growth, which creates new income growth and advances consumer spending. Affordable credit creates another impetus, which propels investments in construction and supports related industries. The performance of the market is forecast to continue with moderate growth, with an anticipated CAGR of +X% for the five-year period from 2015 to 2020.

From 2012, the recovery in consumption was supported by import growth that outpaced more moderate production expansion. The strong U.S. dollar enabled foreign companies to improve their positions on the U.S. hardwood veneer and plywood market, boosting the import share in consumption to X% in 2015. The largest shares of imports in U.S. consumption were held by Chinese hardwood veneer and plywood (X%). Indonesia and Canada followed with a X% share each. Moreover, imports from China (+X percentage points) and Canada (+X percentage points) strengthened their positions in the U.S. market between 2008 and 2015.

The U.S. was a net importer of hardwood veneer and plywood. In physical terms, imports consistently exceeded exports from 2007 to 2015. Net U.S. imports of hardwood veneer and plywood have shown a negative trend since 2012. In 2015, this industry ran a significant trade deficit of X million USD. This deficit could grow substantially in the years to come.

Hardwood veneer and plywood manufacturing is still in the recovery phase of the economic cycle. From 2008 to 2015, the U.S. hardwood veneer and plywood manufacturing has displayed fluctuations in value. After a hard drop, domestic production recovered over the period under review, up to 2015.. U.S. hardwood veneer and plywood output increased by X billion USD in 2015. Foreign competition, particularly from China, is expected to continue increasing through to 2020, moderating the industry's growth prospects over the next five years.

While U.S. consumption, imports, and production posted growth, export rates were negative. From 2007 to 2015, U.S. hardwood veneer and plywood exports showed a steady decrease. There was an annual drop of -X% throughout the analysed period. In 2015, the U.S. exported X million USD, which was X% under the previous year.

In 2015, Canada (X% based on USD), Mexico (X%), and Australia (X%) were the main destinations of U.S. hardwood veneer and plywood exports. The shares exported to Mexico (+X percentage points) and Australia (+X percentage points) increased, while the share sent to Canada illustrated negative dynamics (-X percentage points) between 2007 and 2015.

Do you want to know more about the U.S. hardwood veneer and plywood market? Get the latest trends and insight from our report. It includes a wide range of statistics on

- hardwood veneer and plywood market share

- hardwood veneer and plywood prices

- hardwood veneer and plywood industry

- hardwood veneer and plywood sales

- hardwood veneer and plywood market forecast

- hardwood veneer and plywood price forecast

- key hardwood veneer and plywood producers

Source: U.S. Hardwood Veneer And Plywood Market. Analysis And Forecast to 2020

This report provides an in-depth analysis of the market for hardwood veneer and plywood in the U.S.. Within it, you will discover the latest data on market trends and opportunities by country, consumption, production and price developments, as well as the global trade (imports and exports). The forecast exhibits the market prospects through 2030.

Product coverage:

- NAICS 321211 - Hardwood veneer and plywood manufacturing

Companies mentioned:

- Columbia Forest Products

- Smith Family Companies

- Veneer Technologies

- States Industries

- Decorative Panels International

- Mt. Baker Products

- Rutland Plywood Corp.

- The Freeman Corporation

- Marion Plywood Corporation

- David R. Webb Company

- Nmsa

- International Timber and Veneer

- Miller Veneers

- Amos-Hill Associates

- Swaner Hardwood Co.

- Manthei

- Murphy Company

- Ferche Millwork

- Standard Plywoods Incorporated

- Swanson Group Mfg.

- Coldwater Veneer

- Birchwood Lumber & Veneer Co.

- Plycraft Industries

- Bessemer Plywood Corp.

- Davis Wood Products

- Timber Products Michigan Limited Partnership

- Danzer Services

- Northern Michigan Veneers

- Columbia Plywood Corporation

- Plum Creek Northwest Plywood

- Coastal Plywood Company

- Ivc USA Inc.

Country coverage:

- United States

Data coverage:

- Market volume and value

- Per Capita consumption

- Forecast of the market dynamics in the medium term

- Trade (exports and imports) in the U.S.

- Export and import prices

- Market trends, drivers and restraints

- Key market players and their profiles

Reasons to buy this report:

- Take advantage of the latest data

- Find deeper insights into current market developments

- Discover vital success factors affecting the market

This report is designed for manufacturers, distributors, importers, and wholesalers, as well as for investors, consultants and advisors.

In this report, you can find information that helps you to make informed decisions on the following issues:

- How to diversify your business and benefit from new market opportunities

- How to load your idle production capacity

- How to boost your sales on overseas markets

- How to increase your profit margins

- How to make your supply chain more sustainable

- How to reduce your production and supply chain costs

- How to outsource production to other countries

- How to prepare your business for global expansion

While doing this research, we combine the accumulated expertise of our analysts and the capabilities of artificial intelligence. The AI-based platform, developed by our data scientists, constitutes the key working tool for business analysts, empowering them to discover deep insights and ideas from the marketing data.

-

1. INTRODUCTION

Making Data-Driven Decisions to Grow Your Business

- REPORT DESCRIPTION

- RESEARCH METHODOLOGY AND AI PLATFORM

- DATA-DRIVEN DECISIONS FOR YOUR BUSINESS

- GLOSSARY AND SPECIFIC TERMS

-

2. EXECUTIVE SUMMARY

A Quick Overview of Market Performance

- KEY FINDINGS

- MARKET TRENDS This Chapter is Available Only for the Professional Edition PRO

-

3. MARKET OVERVIEW

Understanding the Current State of The Market and Its Prospects

- MARKET SIZE

- MARKET STRUCTURE

- TRADE BALANCE

- PER CAPITA CONSUMPTION

- MARKET FORECAST TO 2030

-

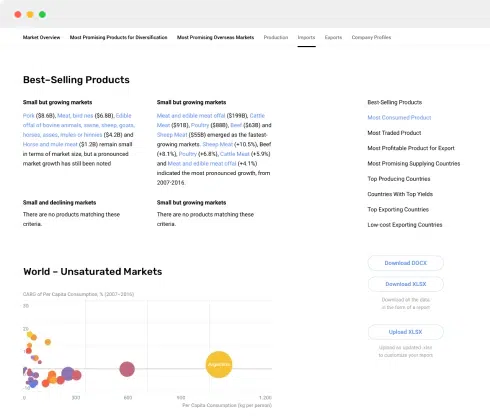

4. MOST PROMISING PRODUCT

Finding New Products to Diversify Your Business

This Chapter is Available Only for the Professional Edition PRO- TOP PRODUCTS TO DIVERSIFY YOUR BUSINESS

- BEST-SELLING PRODUCTS

- MOST CONSUMED PRODUCT

- MOST TRADED PRODUCT

- MOST PROFITABLE PRODUCT FOR EXPORT

-

5. MOST PROMISING SUPPLYING COUNTRIES

Choosing the Best Countries to Establish Your Sustainable Supply Chain

This Chapter is Available Only for the Professional Edition PRO- TOP COUNTRIES TO SOURCE YOUR PRODUCT

- TOP PRODUCING COUNTRIES

- TOP EXPORTING COUNTRIES

- LOW-COST EXPORTING COUNTRIES

-

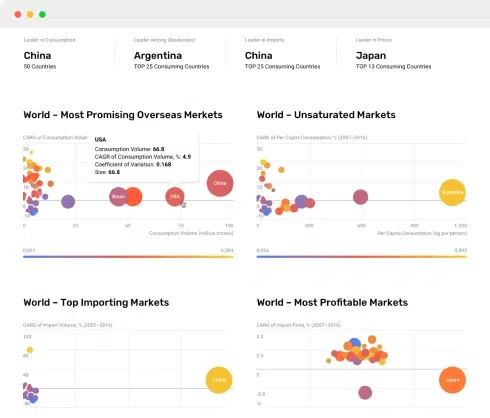

6. MOST PROMISING OVERSEAS MARKETS

Choosing the Best Countries to Boost Your Exports

This Chapter is Available Only for the Professional Edition PRO- TOP OVERSEAS MARKETS FOR EXPORTING YOUR PRODUCT

- TOP CONSUMING MARKETS

- UNSATURATED MARKETS

- TOP IMPORTING MARKETS

- MOST PROFITABLE MARKETS

7. PRODUCTION

The Latest Trends and Insights into The Industry

- PRODUCTION VOLUME AND VALUE

8. IMPORTS

The Largest Import Supplying Countries

- IMPORTS FROM 2012–2023

- IMPORTS BY COUNTRY

- IMPORT PRICES BY COUNTRY

9. EXPORTS

The Largest Destinations for Exports

- EXPORTS FROM 2012–2023

- EXPORTS BY COUNTRY

- EXPORT PRICES BY COUNTRY

-

10. PROFILES OF MAJOR PRODUCERS

The Largest Producers on The Market and Their Profiles

This Chapter is Available Only for the Professional Edition PRO -

LIST OF TABLES

- Key Findings In 2023

- Market Volume, In Physical Terms, 2012–2023

- Market Value, 2012–2023

- Per Capita Consumption In 2012-2023

- Imports, In Physical Terms, By Country, 2012–2023

- Imports, In Value Terms, By Country, 2012–2023

- Import Prices, By Country Of Origin, 2012–2023

- Exports, In Physical Terms, By Country, 2012–2023

- Exports, In Value Terms, By Country, 2012–2023

- Export Prices, By Country Of Destination, 2012–2023

-

LIST OF FIGURES

- Market Volume, In Physical Terms, 2012–2023

- Market Value, 2012–2023

- Market Structure – Domestic Supply vs. Imports, In Physical Terms, 2012-2023

- Market Structure – Domestic Supply vs. Imports, In Value Terms, 2012-2023

- Trade Balance, In Physical Terms, 2012-2023

- Trade Balance, In Value Terms, 2012-2023

- Per Capita Consumption, 2012-2023

- Market Volume Forecast to 2030

- Market Value Forecast to 2030

- Products: Market Size And Growth, By Type

- Products: Average Per Capita Consumption, By Type

- Products: Exports And Growth, By Type

- Products: Export Prices And Growth, By Type

- Production Volume And Growth

- Exports And Growth

- Export Prices And Growth

- Market Size And Growth

- Per Capita Consumption

- Imports And Growth

- Import Prices

- Production, In Physical Terms, 2012–2023

- Production, In Value Terms, 2012–2023

- Imports, In Physical Terms, 2012–2023

- Imports, In Value Terms, 2012–2023

- Imports, In Physical Terms, By Country, 2023

- Imports, In Physical Terms, By Country, 2012–2023

- Imports, In Value Terms, By Country, 2012–2023

- Import Prices, By Country Of Origin, 2012–2023

- Exports, In Physical Terms, 2012–2023

- Exports, In Value Terms, 2012–2023

- Exports, In Physical Terms, By Country, 2023

- Exports, In Physical Terms, By Country, 2012–2023

- Exports, In Value Terms, By Country, 2012–2023

- Export Prices, By Country Of Destination, 2012–2023