U.S. Adhesive Market. Analysis And Forecast to 2030

Get instant access to more than 2 million reports, dashboards, and datasets on the IndexBox Platform.

View PricingAdhesive Market - Consumption Growth Amidst Environmental Restrictions for Manufacturers

Photo: © kenny001 / Bigstockphoto

Curbs on emissions are bringing about changes in the commodity pattern of the U.S. adhesives industry.

In 2015, U.S. adhesives consumption continued to grow; this positive trend started after the culmination of the global recession seven years ago. Against the 2014 figure, it has increased by X% in value terms (to $X billion) and by X%, when compared with the 2008 figure. The recovery seen in the consumer industries - construction and car manufacturing - is the driving factor behind this growth.

The U.S. adhesive market is loosely dependent on imports from abroad: from 2010-2015, the imports share in terms of consumption did not exceed X%. The imports structure was dominated by products from Canada (in value terms, Canada accounted for X% of the adhesives imported into the USA in 2015); Germany was in second place (X%), followed by Mexico (X%) and China (X%). Canada and Mexico are also amongst the largest importers of U.S. manufactured adhesives, due to their geographical proximity and the supportive trading conditions: in 2015, their share in U.S. exports amounted to X% and X%, respectively.

From 2010-2015, the exports share oscillated around the X% of the domestic adhesives output. The U.S. share in terms of global adhesives exports remained stable: this figure stood at X% in 2010 and at X% in 2015, second in the world after Germany; Germany's share did not fall below X% for the same period.

From 2007-2015, U.S. adhesives production escalated at an average annual rate of X%, reaching $X billion, based on last year's results. At the same time, the output commodity pattern showed signs of instability. According to IndexBox estimates, the share of natural based glues and adhesives in terms of U.S. production increased from X% to X% over the period from 2008-2014 (Figure X), while the share of synthetic resins and rubber adhesives contracted from X% to X% over the same period. These changes are a result of the actions of the regulatory authorities, restricting the use of products that produce toxic waste and exert a negative impact on the environment. In the future, this is set to result in the increased production of bioadhesives, which use natural raw materials in the production process (e.g. starch and natural rubber), instead of synthetic polymers (silicones, vinyl, acrylic). The transition from the production of traditional solvent-based adhesives to their water-based alternatives would also be another consequence of this.

IndexBox analysts maintain that the adhesive market is set to experience measured growth in the medium term. Enhanced demand from the car manufacturing and construction sectors, combined with increased employment levels and rising household incomes, not to mention the development of innovative technology, which will extend the potential scope of use for adhesives, will be the driving impulses for the sector's steady expansion.

Do you want to know more about the U.S. adhesive market? Get the latest trends and insight from our report. It includes a wide range of statistics on

- adhesive market share

- adhesive prices

- adhesive industry

- adhesive sales

- adhesive market forecast

- adhesive price forecast

- key adhesive producers

This report provides an in-depth analysis of the adhesive market in the U.S.. Within it, you will discover the latest data on market trends and opportunities by country, consumption, production and price developments, as well as the global trade (imports and exports). The forecast exhibits the market prospects through 2030.

Product coverage:

- NAICS 325520 - Adhesive manufacturing

Companies mentioned:

- Saint-Gobain Corporation

- Lord Corporation

- H.B. Fuller Company

- Tremco Incorporated

- Morton Salt

- Rogers Corporation

- Mapei Corporation

- Fairmount Santrol Inc.

- Bostik

- Elmer's Products

- Dap Products Inc.

- Adhesives Research

- Sika Corporation

- Royal Adhesives and Sealants LLC

- Whitford Worldwide Company

- Stahl (usa) Inc.

- C.W. Matthews Contracting Co.

- Ips Corporation

- Custom Building Products

- Morgan Adhesives Company

- Adco Global

- Morton International

- PRC - Desoto International

- Sanford

- Indopco

- National Starch and Chemical Holding Corporation

- Berwind Consumer Products

- DSM Finance USA Inc.

- Covalence Specialty Adhesives

- Royal Holdings

- DSM Holding Company Usa

- Lj/Hah Holdings Corporation

- Rust-Oleum Corporation

Country coverage:

- United States

Data coverage:

- Market volume and value

- Per Capita consumption

- Forecast of the market dynamics in the medium term

- Trade (exports and imports) in the U.S.

- Export and import prices

- Market trends, drivers and restraints

- Key market players and their profiles

Reasons to buy this report:

- Take advantage of the latest data

- Find deeper insights into current market developments

- Discover vital success factors affecting the market

This report is designed for manufacturers, distributors, importers, and wholesalers, as well as for investors, consultants and advisors.

In this report, you can find information that helps you to make informed decisions on the following issues:

- How to diversify your business and benefit from new market opportunities

- How to load your idle production capacity

- How to boost your sales on overseas markets

- How to increase your profit margins

- How to make your supply chain more sustainable

- How to reduce your production and supply chain costs

- How to outsource production to other countries

- How to prepare your business for global expansion

While doing this research, we combine the accumulated expertise of our analysts and the capabilities of artificial intelligence. The AI-based platform, developed by our data scientists, constitutes the key working tool for business analysts, empowering them to discover deep insights and ideas from the marketing data.

-

1. INTRODUCTION

Making Data-Driven Decisions to Grow Your Business

- REPORT DESCRIPTION

- RESEARCH METHODOLOGY AND AI PLATFORM

- DATA-DRIVEN DECISIONS FOR YOUR BUSINESS

- GLOSSARY AND SPECIFIC TERMS

-

2. EXECUTIVE SUMMARY

A Quick Overview of Market Performance

- KEY FINDINGS

- MARKET TRENDS This Chapter is Available Only for the Professional Edition PRO

-

3. MARKET OVERVIEW

Understanding the Current State of The Market and Its Prospects

- MARKET SIZE

- MARKET STRUCTURE

- TRADE BALANCE

- PER CAPITA CONSUMPTION

- MARKET FORECAST TO 2030

-

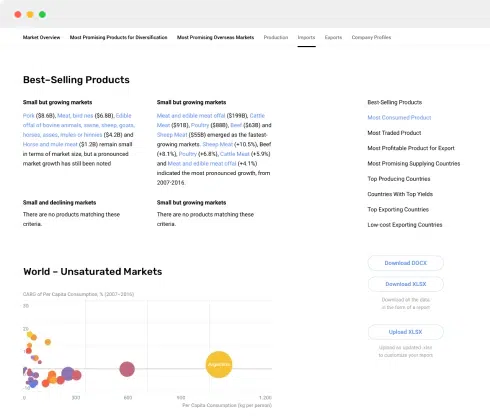

4. MOST PROMISING PRODUCT

Finding New Products to Diversify Your Business

This Chapter is Available Only for the Professional Edition PRO- TOP PRODUCTS TO DIVERSIFY YOUR BUSINESS

- BEST-SELLING PRODUCTS

- MOST CONSUMED PRODUCT

- MOST TRADED PRODUCT

- MOST PROFITABLE PRODUCT FOR EXPORT

-

5. MOST PROMISING SUPPLYING COUNTRIES

Choosing the Best Countries to Establish Your Sustainable Supply Chain

This Chapter is Available Only for the Professional Edition PRO- TOP COUNTRIES TO SOURCE YOUR PRODUCT

- TOP PRODUCING COUNTRIES

- TOP EXPORTING COUNTRIES

- LOW-COST EXPORTING COUNTRIES

-

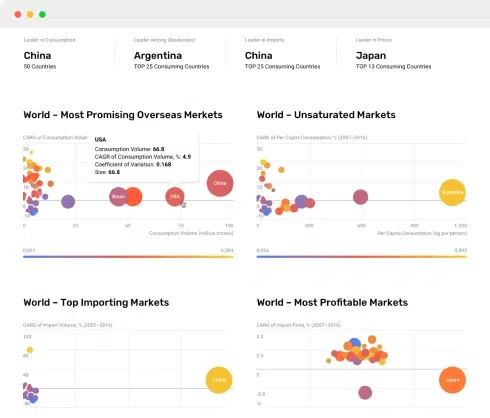

6. MOST PROMISING OVERSEAS MARKETS

Choosing the Best Countries to Boost Your Exports

This Chapter is Available Only for the Professional Edition PRO- TOP OVERSEAS MARKETS FOR EXPORTING YOUR PRODUCT

- TOP CONSUMING MARKETS

- UNSATURATED MARKETS

- TOP IMPORTING MARKETS

- MOST PROFITABLE MARKETS

7. PRODUCTION

The Latest Trends and Insights into The Industry

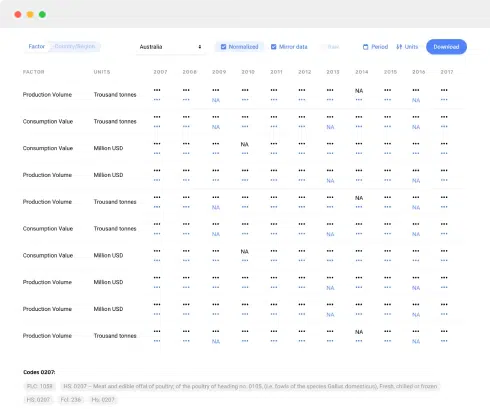

- PRODUCTION VOLUME AND VALUE

8. IMPORTS

The Largest Import Supplying Countries

- IMPORTS FROM 2012–2023

- IMPORTS BY COUNTRY

- IMPORT PRICES BY COUNTRY

9. EXPORTS

The Largest Destinations for Exports

- EXPORTS FROM 2012–2023

- EXPORTS BY COUNTRY

- EXPORT PRICES BY COUNTRY

-

10. PROFILES OF MAJOR PRODUCERS

The Largest Producers on The Market and Their Profiles

This Chapter is Available Only for the Professional Edition PRO -

LIST OF TABLES

- Key Findings In 2023

- Market Volume, In Physical Terms, 2012–2023

- Market Value, 2012–2023

- Per Capita Consumption In 2012-2023

- Imports, In Physical Terms, By Country, 2012–2023

- Imports, In Value Terms, By Country, 2012–2023

- Import Prices, By Country Of Origin, 2012–2023

- Exports, In Physical Terms, By Country, 2012–2023

- Exports, In Value Terms, By Country, 2012–2023

- Export Prices, By Country Of Destination, 2012–2023

-

LIST OF FIGURES

- Market Volume, In Physical Terms, 2012–2023

- Market Value, 2012–2023

- Market Structure – Domestic Supply vs. Imports, In Physical Terms, 2012-2023

- Market Structure – Domestic Supply vs. Imports, In Value Terms, 2012-2023

- Trade Balance, In Physical Terms, 2012-2023

- Trade Balance, In Value Terms, 2012-2023

- Per Capita Consumption, 2012-2023

- Market Volume Forecast to 2030

- Market Value Forecast to 2030

- Products: Market Size And Growth, By Type

- Products: Average Per Capita Consumption, By Type

- Products: Exports And Growth, By Type

- Products: Export Prices And Growth, By Type

- Production Volume And Growth

- Exports And Growth

- Export Prices And Growth

- Market Size And Growth

- Per Capita Consumption

- Imports And Growth

- Import Prices

- Production, In Physical Terms, 2012–2023

- Production, In Value Terms, 2012–2023

- Imports, In Physical Terms, 2012–2023

- Imports, In Value Terms, 2012–2023

- Imports, In Physical Terms, By Country, 2023

- Imports, In Physical Terms, By Country, 2012–2023

- Imports, In Value Terms, By Country, 2012–2023

- Import Prices, By Country Of Origin, 2012–2023

- Exports, In Physical Terms, 2012–2023

- Exports, In Value Terms, 2012–2023

- Exports, In Physical Terms, By Country, 2023

- Exports, In Physical Terms, By Country, 2012–2023

- Exports, In Value Terms, By Country, 2012–2023

- Export Prices, By Country Of Destination, 2012–2023